The future's uncertain and the end is always near

Yesterday, the monthly consumer price index report, which measures inflation, came out and showed that inflation for December was negative. That is six months in a row now where inflation has slowed down compared to where it was during the first half of 2022. While annual inflation is still much higher than the 2% target the Fed has, it is, as of now, trending in the right direction. At the same time, the job market is as strong as ever with unemployment at 3.5%, tied for the lowest it has been since 1969.

The US economy, to say nothing of the global economy, has been through a lot over the last three years. Last year was definitely one for the record books. So much of what was thought to be known about how the economy works turned out to be wrong, in good and bad ways. You can see what I’m getting at, right? Predicting even the immediate future is hard. Predicting where things will be years from now is a fool’s errand.

Needless to say, I’m not going to make any predictions here. I won’t even bother trying to guess what things will look like in a few months. With respect to the US economy, it is, for now, almost in a goldilocks-type situation. Inflation is still high, but coming down, while unemployment remains low and plenty of jobs are being added each month. If that continues, the Fed will have achieved the proverbial soft landing, where inflation is brought down without causing unemployment to surge. That, too, would be one for the record books.

Just because the trends today are good does not mean they will continue. There is plenty of debate now about how aggressive the Fed should be in trying to tame inflation. Some argue it has done enough and should stop raising interest rates. Others argue it should continue to raise interest rates, but do it at a more modest pace. The latter group has won out for now, but nobody knows how much longer that will last. Everybody wants to achieve a soft landing, but there is no consensus on how best to do it.

Conventional wisdom, i.e., what economists, the Fed and businesses think, has shifted significantly since the second half of 2021. First, inflation was transitory and not something to be too concerned with. Then, inflation was entrenched and a recession was inevitable. Now, it seems conventional wisdom is becoming more open to a soft landing. I have never taken a position on any of that because I have no idea.

We are just not good at predicting large-scale, future events. Some of us have plenty of imagination, but it only goes so far. Our tendency is to stick to our ways, no matter what they are. If something has worked in the past, we stick to it even though it is not guaranteed to work again in the future. If historically X has happened after Y, then we assume that will continue no matter how different the circumstances are.

This here is an example of sticking to the fallacy of looking at past events to make future predictions and not accounting for the different circumstances. It discusses the high vacancy rate in the job market right now and argues that vacancy rates come down before unemployment goes up. The claim is that vacancies will fall, but unemployment will rise afterwards and suggests there is no other possible outcome. In other words, a soft landing cannot happen. The evidence? Nine such episodes going back to the 1950s. The problem? The sample size is very small and none of those episodes dealt with a pandemic or messed up supply chains on a global scale.

That is not to say unemployment will not rise, it very well might. What it is to say is that the world we are in now is markedly different from any world that came before it. Our experience with economic downturns is very limited and our experience with post-pandemic global economies is non-existent. There is nothing wrong with looking at what has happened before, but to do that and assume that whatever has happened before is set in stone and will happen again is a big error.

The subject of the article I linked to has also pointed out that high inflation almost never comes down fast. He cites a study of fifty such episodes in developed countries since 1970 which showed that it takes many years to bring down inflation when it goes above 8%. The idea that inflation could come down as quickly as it went up in 2021 is, as he puts it, “outside the range of normal historical experience.”

That is certainly right, but not necessarily in the way that he thinks it is. If I had to sum up the economy of the last three years in a sentence, “outside the range of normal historical experience” would be it. Almost nothing we have gone through since early 2020 has been within the range of normal historical experience. While we will go through some experiences that we have endured in the past again, there will be plenty of new adventures we will have, good and bad. Anyone who thinks that something that has not happened before can never happen is admitting that they are wedded to their ways, lack an imagination and their mentality is calcified.

In the case of inflation today, take a look at the graph below. You can see that inflation took off in 2021. You can also see that it has started to come down just as fast as it went up. Will that continue? Nobody knows, but to say it is impossible is absurd. Maybe it stalls out or maybe it shoots up again, I don’t know and neither does anyone else. There are reasons to think inflation will keep going down and reasons to think otherwise. We will find out soon enough what happens, but nothing is determined.

The last year and a half has seen so many narratives/ideas turn out to be wrong that it is hard to keep track of them all. Low interest rates are here forever, inflation is a thing of the past, China is the model to emulate, China going into lockdown will send inflation surging, Putin is a genius, Europe will not stand up to Russia, authoritarianism is on the rise, democracy is on the ropes, the US economy is in a recession, there will be a red wave, industrial policy should not be tried and crypto is what the cool people buy are just the biggest ones I can think of off the top of my head. In the next three years, who knows what will happen? All of that could reverse. Let’s hope not, at least for most of those things, but nobody knows for sure.

Today, there are all kinds of narratives/ideas that are ripe for potentially aging poorly. Examples include a recession is inevitable, higher interest rates are here to stay, the days of low inflation are over, globalization is receding and Trump is done for. The most confident of those predictions seems to be about the inevitability of a recession. Most everyone in business and economics seems to believe one will happen this year or next year and that it is set in stone.

If we have a recession, it will be the most anticipated one ever, which will probably be a first. While there is always someone predicting a recession, I have never heard of a recession that followed most people believing it would happen. Recessions tend to happen when conventional wisdom is that everything is wonderful and great. I point that out not to say that a recession will not happen, but to note that conventional wisdom has been wrong repeatedly since 2020 and there is no reason to automatically believe this time is different.

My emphasis is on the economy here, but unforeseen twists and turns happen with most everything. Life is a random walk. It is not linear and past is not prologue. Not everything can be reduced to statistical models and mathematical equations. There are plenty of things that can be quantified, but human psychology isn't one of them. People make all kinds of hugely consequential decisions for reasons that can’t be explained by math or logic.

When trying to plan for the future, I find that there are two people whose words of wisdom are timeless. They are not economists, financial gurus, statisticians or anything of the sort. They are Yogi Berra and Mike Tyson. Yogi Berra, known for his sayings almost as much as for baseball, famously said “it’s tough to make predictions, especially about the future.” Mike Tyson famously said, “everyone has a plan, until they get punched in the mouth.” I don’t think the takeaway from those quotes should be that planning is futile, but that planning should be done with humility and with the recognition that not everything will go the way you think. Anyone making plans should be ready, willing and able to change course when that happens.

We have to recognize and appreciate that our knowledge is very limited. For example, when it comes to economic data, i.e., inflation and unemployment statistics, that has only been comprehensively provided since around 1945. That is a long time, but not that long. Plenty happened before then that we do not have much of a record of. No period from 1945-2020 dealt with what we are dealing with now.

The world economy involves billions of people and tons of moving parts and feedback loops. All of those interact in ways that make intuitive sense, but also in ways that do not. The world is as interconnected as it has ever been. What happens in one part of the world can have huge effects in places thousands of miles away that nobody there was thinking about because they had no reason to.

An example of that is one of the indirect effects of Russia invading Ukraine. The war has directly involved Russia and Ukraine, but has also involved the west imposing sanctions on Russia in response to the invasion. Since the invasion, Russia has blocked Ukraine from exporting grains, which it is a big supplier of. One outcome of that has been a famine in parts of Africa and the Middle East where no country is directly involved in the war and not many have imposed sanctions on Russia. I highly doubt many people there anticipated that one of the outcomes of a war a long way away from them that they have nothing to do with would be a major crisis where they live, but that is what has happened.

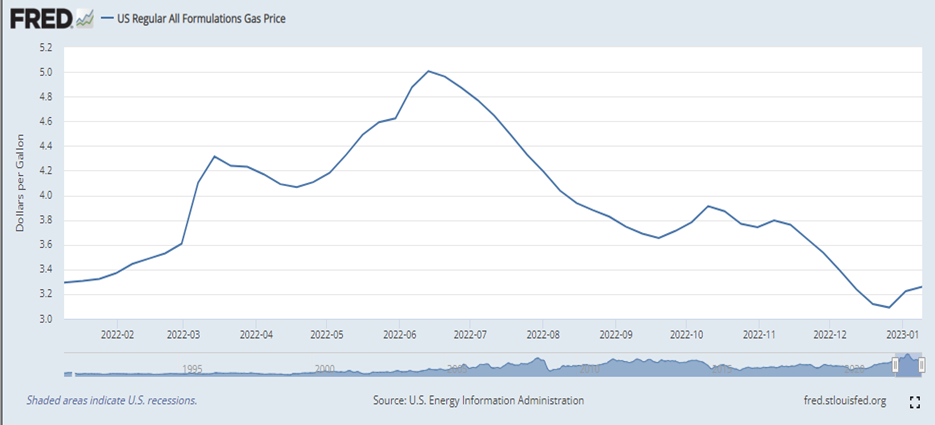

Another example was the surge in gas prices in the US that happened after the invasion. That was a more predictable outcome, but it has been a wild ride for the last year, as you can see from the graph below. When Russia first invaded Ukraine, gas prices surged, then plateaued, then surged again and have since plummeted. Gas prices went from a little over $3.20 a gallon in February 2022 to $5 a gallon in June and now are back where they were a year ago. If there is a single person on planet earth who predicted all that would happen, I would like to meet them.

There was a belief that oil prices could hit $200 a barrel depending on how tough sanctions imposed on Russia were. Plenty of sanctions have been imposed on Russia and there is an oil price cap in place now against Russian oil exports. But $200 a barrel has not come to pass and it seems, for now, that the oil price cap is working. The big worry was that a large chunk of Russian oil would be pulled off the market entirely, but that has not happened. Maybe it does happen, but who knows?

Moving to US politics, while it is more predictable than the US or global economy, it is still full of surprises. There have been plenty of twists and turns that looked impossible ten years ago. The biggest example is Trump getting nominated and elected president, but there have been many others as well. Democrats did very well in the midterms last year when almost everyone thought they would get wiped out. Historically, Democrats don’t win runoffs in Georgia, but have now won three in a row. In the past, Democrats have had problems with their voters being heavily concentrated in a few areas, putting them at a disadvantage in the House. Now, it looks like it is Republicans who have that problem. Is that an enduring feature or just an artifact of current party coalitions? My guess is the latter, but we can’t know for sure right now.

Which party will be in the White House in ten years? Which party will control Congress? Which party will be more dominant on the state level? Because we only have two parties, it is much easier to guess the answer, but it is still just a guess. States that are swing states today may wind up becoming reliably red or blue in the future. Conversely, states that are blue or red today may be swing states in the future. There are parts of the country today that are reliably blue that used to be reliably red and vice-versa. That will almost certainly be true of other places in the future, but it is hard to know exactly where and when that will happen. My guess is that the trend of suburban areas getting bluer while rural areas get redder will continue, but that may not pan out.

Who wins elections and gets to govern is influenced by events beyond elected officials’ control, even though it can radically change the course of history. FDR was the most consequential president of the 20th century, but he also benefited from good timing. The economy collapsed on Herbert Hoover’s watch, which discredited the Republican Party for a generation. Neither Hoover nor the Republican Party caused the Great Depression nor could they have done anything to stop it from happening, but it happened when they were in charge and they paid a huge price for it. Because Democrats dominated for so long, we got the New Deal and the modern administrative state. Programs and laws from the New Deal that are still with us today include Social Security, the SEC, the NLRB, the federal minimum wage and the FDIC.

Ronald Reagan was a consequential president, too, but had he beaten Gerald Ford in the Republican primary in 1976, he either would have lost the general election or he would have been the one presiding over stagflation and dealing with national malaise. Rather than being worshipped by every Republican today and cited enviously by Democrats, he might have met the same end as Jimmy Carter. Carter did not cause stagflation, but his perceived mishandling of it did him in and ended the New Deal coalition that had been around since the 1930s. We are not entirely living in the world Reagan built today, but we are not entirely out of it either.